If you’re facing financial hardship, your mortgage lender might offer mortgage forbearance as one of the options to help with your situation. This is one of the solutions lenders offer, but it’s not right for everyone.

Understanding how it works will help you decide if the choice is right for you or if you should explore other options.

What is Mortgage Forbearance?

Mortgage forbearance is a short-term plan to help homeowners during a financial crisis. For example, if you lost your job or fell ill and cannot make your mortgage payments, your lender may offer a forbearance plan.

This plan is a temporary halt to your mortgage payments, or some plans offer a reduced payment for a short period. It’s meant to help you get back on your feet while avoiding foreclosure.

A forbearance agreement works best when you’re sure your situation is temporary and when you know you can make up the difference in the deferred payments.

How Does Mortgage Forbearance Work?

Every lender has different options when it comes to a forbearance agreement, but the common options include the following:

Payment pause – A lender may allow you to stop making mortgage payments for a few months. The length of the agreement depends on the circumstances and what the lender allows. It can be a few months or longer; however, interest continues to accrue.

Lower payments – If you can afford partial payments, your lender may cut your payments down temporarily. How much they cut them down varies by lender and your personal situation.

Remember, neither option is permanent, and you’ll eventually have to make up the missed payments.

What Happens After the Mortgage Forbearance Agreement?

The forbearance agreement doesn’t last forever, and once it ends, you must pick up where you left off, but that still leaves the payments you didn’t make.

Just like the forbearance term, how each lender handles what happens after the agreement differs. Here are some of the most common options.

Lump Sum Payment

With the lump sum payment agreement, you must pay the total amount of payments deferred during the agreement.

For example, if you deferred $1,000 a month for six months, you must pay $6,000 at the end of the agreement.

This isn’t ideal for most people since you enter a forbearance agreement because you can’t afford your payments. However, if there’s a chance you’ll receive a windfall before the agreement ends, you can choose this option and pay back everything you owe at once.

Spread the Payments Out

The most common option is to spread out the payments you skipped. For example, if you skipped $10,000 in mortgage payments, your lender may spread the amount out over 12 months, adding $833 to your existing mortgage payment.

This method only works if you’re back on your feet and have extra room in your budget for a larger mortgage payment.

Extend the Loan’s Term

Some lenders allow you to track the amount owed at the end of your loan term and will extend the term for the number of months you skipped. For example, if you skipped eight months of payments, they’ll extend your term by eight months.

This is usually the easiest option because it doesn’t require a lump sum payment or a higher mortgage payment each month.

Mortgage Forbearance Plan vs. Loan Modification

Understanding the difference between mortgage forbearance and loan modification is important.

As discussed above, a mortgage forbearance is temporary and depends on your circumstances. A loan modification is a permanent change to your mortgage agreement. Lenders have options when changing your loan terms to make them more affordable. They include:

Writing off a percentage of your principal balance to make your payments lower

Reducing your interest rate to make your payments lower

Extending your loan term to reduce your monthly payments

A loan modification is an agreement you must sign and have notarized, and that gets recorded with the county, replacing your existing mortgage agreement.

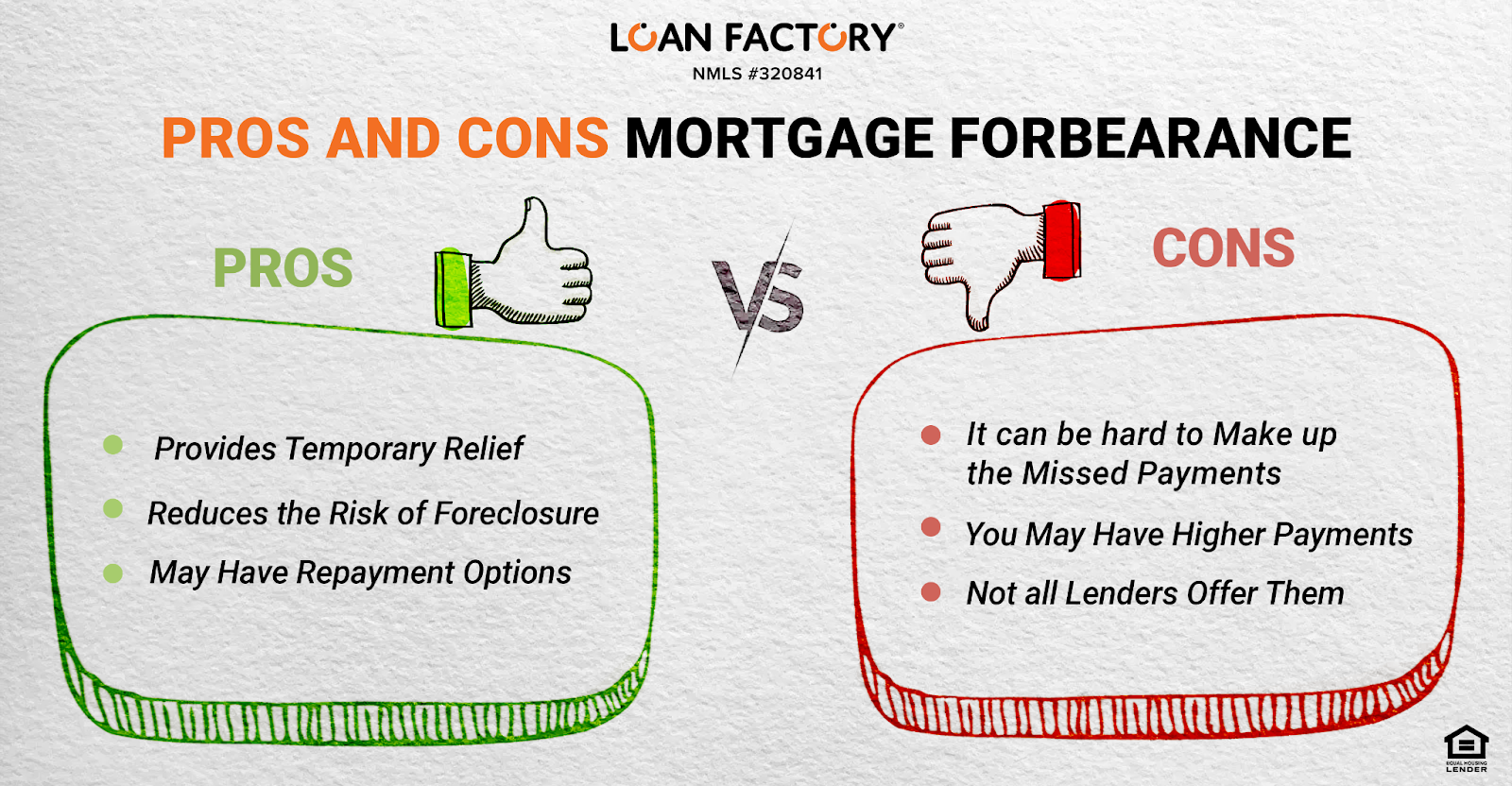

Pros and Cons Mortgage Forbearance

A mortgage forbearance agreement has pros and cons. Here’s what you should know.

Pros:

Provides Temporary Relief

If your situation is temporary, you might need a quick break from your mortgage payments. Then, when you’re back on your feet, you can pick up where you left off and not risk losing your home. It can be a good way to get through a spell of unemployment or an unexpected illness.

Reduces the Risk of Foreclosure

When you have a forbearance agreement, you increase the chances of keeping your home. As long as you meet the terms of the agreement, you won’t lose your home.

May Have Repayment Options

There are different repayment options that vary by lender. As long as you’re honest with your lender about what you can afford, they will likely work with you.

Cons:

It can be hard to Make up the Missed Payments

If your lender doesn’t allow term extensions, it can be hard to make up your missed payments which can put your home at risk.

You May Have Higher Payments

If your lender requires you to spread the missed payments over a certain term, it increases your mortgage payment. This can make it harder to afford your payments, putting you at risk of falling behind.

Not all Lenders Offer Them

Not all lenders offer forbearance agreements; if they do, it can be hard to qualify for one.

Final Thoughts

A forbearance agreement can help you when you’re having financial trouble. The key is, to be honest with your lender and not wait until you are a few months behind.

Approach your lender with the situation you have as soon as you know about it, and see what options they offer. Most lenders will work with you because they don’t want to take your home to foreclosure.

Always talk to your lender about options, including loan modification and forbearance, to determine which makes the most sense for your situation.